How Can Kernel Funds Fit Together?

Whether you're new to investing or a seasoned pro, now you can build a portfolio of low-cost, well-d...

Stephen Upton

22 September 2023

Have you ever thought about why on earth a garden variety word is used in the world of finance and investing? Well, from Anglo-Saxon times, a 'hedge' has been a green boundary between pieces of land. 'Hedging' or 'hedging in' your property protects it. From the late 17th century, 'to hedge' meant to protect your stake in gambling by betting on the other side.

Now that we have established where the word originates from and what it means, how does this relate to the world of investing?

When you picture a hedge in front of a property it’s been put there as a means of protection. The same concept applies to hedging investments. In essence, it’s when someone tries to mitigate or reduce risk and protect oneself from loss on some sort of transaction.

Paying insurance is a perfect example of a non-investment hedge. We purchase travel insurance before going on a trip to gain control over what could result in an unpredictable situation. We travel with the hope that nothing bad happens when we embark on a trip, but anything from an injury to stolen property can take place. Insurance helps you hedge your bets so you incur as little loss as possible in an unfortunate situation.

Hedging is a term that comes up in all areas of life. Though, in today’s world, the most prominent setting is within the world of money and investing.

There are many different hedging strategies, but we will focus on currency hedging as this type of hedging is the most common strategy used by fund managers (such as Kernel).

Many investors diversify their investments and gain exposure to overseas markets through funds. One inevitable risk which can come with global investing is foreign exchange (currency) fluctuations – a rise or fall in the value of the NZD, against other currencies, can affect the value of your investments and returns.

A currency-hedged fund is one where the fund manager has hedged out the impact of the currency on investors' returns, meaning that the return you ultimately receive in NZD is the return of the underlying investments in the fund.

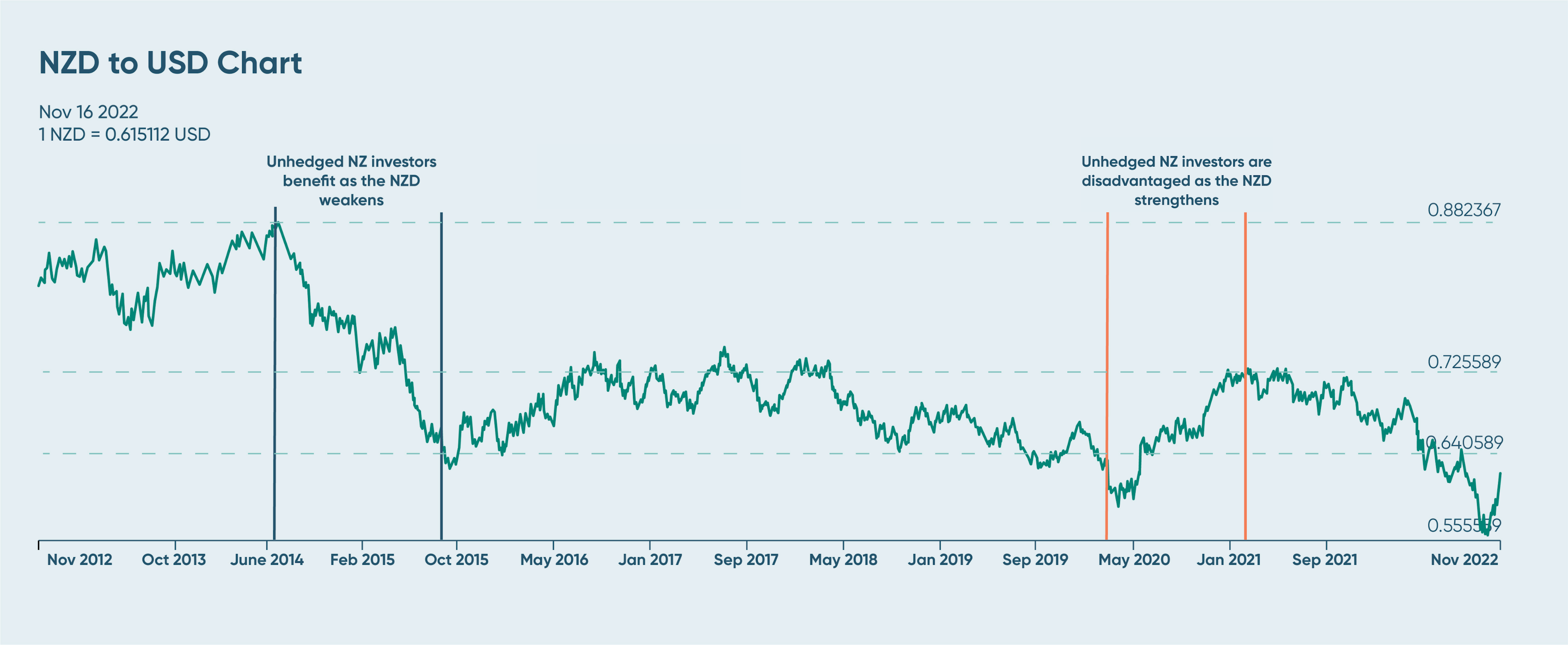

The movement of the NZD/USD over the past year has been significant and has at times showcased incredible volatility. Looking at the S&P 500 index fund as an example, if you were to invest in an unhedged version of this fund you would be impacted by both the underlying investment performance as well as the exchange rate fluctuations between the NZD and USD.

In contrast, the Kernel S&P 500 Fund is priced in NZD and currency hedged to NZD. This means that it will deliver a similar return to the S&P 500 index in USD terms but it won’t be impacted as much by the exchange rate fluctuations between the NZD and USD.

*Assuming the value of the assets in an unhedged fund didn’t change.

Below is a chart that showcases 2 periods when it would be beneficial and disadvantageous to be invested in an unhedged S&P 500 fund.

More recently, this volatility can be seen between November 2021- October 2022 as the NZD declined ~20% against the USD during that period, before strengthening 13%.

Money King NZ have written a great piece on the performance impact of hedging and explaining the differences between hedged and unhedged returns using different S&P 500 index funds if you’d like to learn more.

The appeal for hedging can be for simple reasons such as some investors may argue that they just want to invest in the underlying assets of the fund, and not experience the additional risks of currency movements.

Additionally, it can also help clarify confusion in returns for some investors. E.g., if you were to invest in the NZD hedged Kernel S&P 500 and the S&P 500 index were to go up 1.00% for the day, your investment should also be up around 1.00%, as the effect of currency is minimised.

When thinking about the disadvantages of hedging, one can sometimes be its complexity. In addition, keeping your investments unhedged has historically helped during periods of economic stress, which has been the case in 2022. The USD strengthened during most of the year and therefore dampened the losses of underlying shares.

Currency hedging can also sometimes incur higher costs, such as higher management fees. This is not the case with Kernel, where our hedged and unhedged international funds have the same fees.

Something else to watch out for is currency hedging policies with different fund managers. Some funds have active currency hedging where the fund manager continually changes the amount of currency hedged within the fund (i.e., moving from 60% hedged currency to, 70%or 100%). This means that investors can lose a sense of control.

At Kernel, we offer 100% currency-hedged options such as the Hedged Global 100, Hedged Global Infrastructure and S&P 500 funds.

As mentioned earlier, Kernel offers a few currency hedged funds that investors can choose from. Generally speaking, NZD-hedged funds can be an option for investors looking to generate returns solely from the underlying investments of the fund. This can be beneficial during times when the NZD is appreciating in value against other currencies.

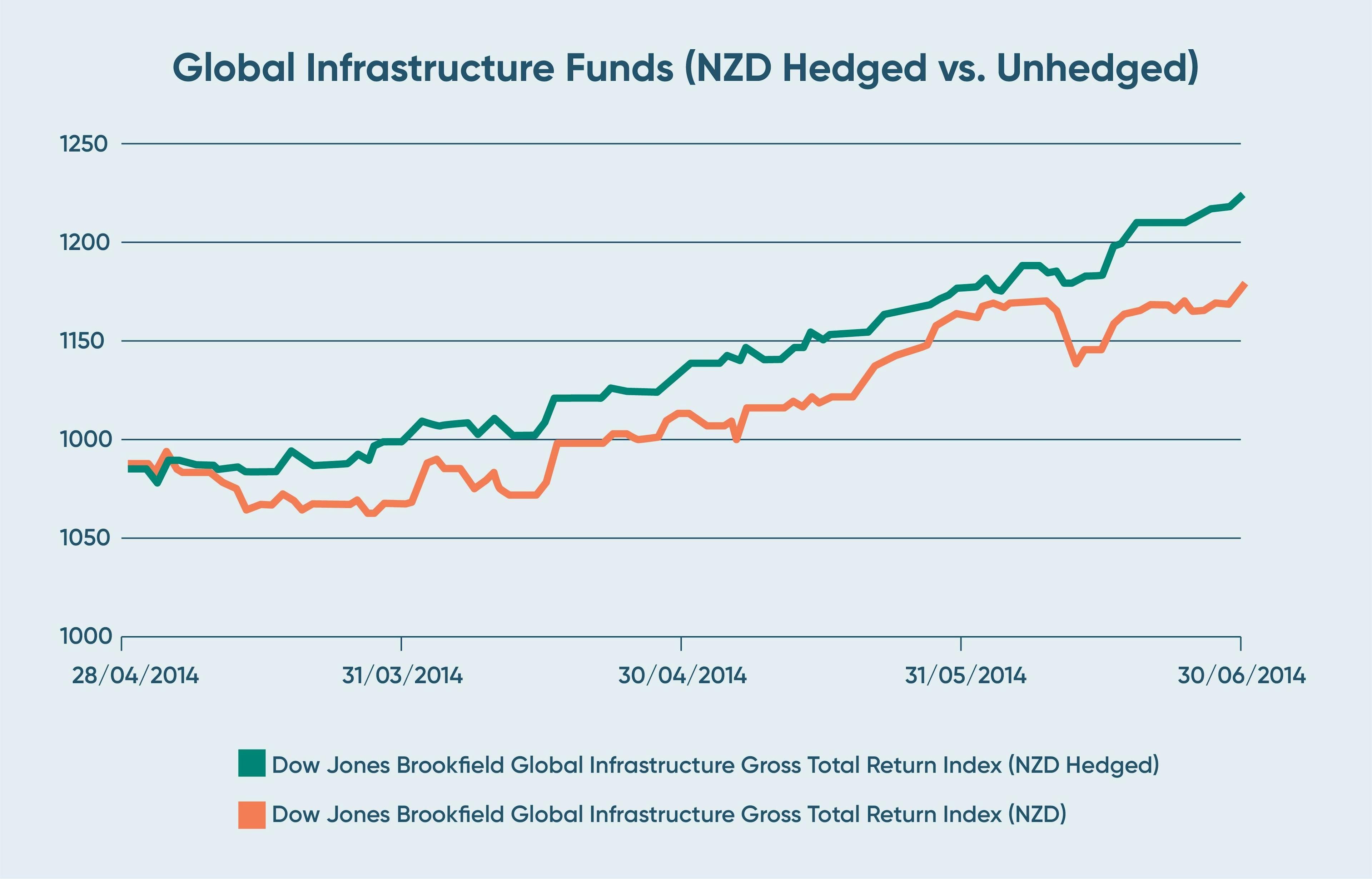

For example, if you were invested in an unhedged version of the Global Infrastructure Fund, and the NZD appreciated against other currencies the value of your investment would decrease as you would receive less in NZD if you decided to sell them.

In this case, the NZD-hedged version of the Global Infrastructure fund would tend to outperform its unhedged counterpart as shown in the figure below (in 6 months from 28 February 2014 to 30 June 2014, NZD went up 4.2% relative to USD).

However, the downside is that during periods when foreign exchange movement might increase the value of your investment, you will not receive this upside potential if you are in an NZD-hedged fund.

So, should you go with a hedged or unhedged fund? Unfortunately, volatility is here to stay, especially in the short term. Remember, nobody can predict or time the market perfectly – which also applies to predicting the movements of foreign exchange rates! Constantly switching from fund to fund to try and pick the most favourable currency at a given time simply won’t work for you over the long term.

Ultimately, the choice to be fully currency hedged, fully unhedged or a mix of both is completely up to you. But remember, your investment decisions should always align with your personal circumstances and financial goals. If in doubt, seek professional advice before making any decisions.

How Can Kernel Funds Fit Together?

Whether you're new to investing or a seasoned pro, now you can build a portfolio of low-cost, well-d...

Stephen Upton

22 September 2023

How to Prioritise Your Financial Goals

Want to improve your financial situation but not sure how where to start? Check out the Kernel guide...

Ben Tutty

6 October 2022

How to Start Investing: Part One

Successful investing isn’t as hard as you think. In this blog we walk you through key concepts and h...

Dean Anderson

13 August 2020

For market updates and the latest news from Kernel, subscribe to our newsletter. Guaranteed goodness, straight to your inbox.

Indices provided by: S&P Dow Jones Indices