Reverse engineer your goals by starting with the bigger picture and breaking it down. Want to know m...

Catherine Emerson

19 January 2020

When it comes to personal finances, debt is a sensitive topic. Many find having debt can leave them feeling overwhelmed, stressed, and unable to get a head, while others are far more secure and not afraid to load up on borrowed money.

Debt is a subject that is often not discussed amongst family and friends and this lack of communication can impact our attitude towards debt. So how are you to know when to pay off debt or do something else with your money? While the compulsion to get out of the red is entirely reasonable, the truth about what exactly you should do with your extra cash is a little more complicated.

In certain situations, it can be smarter to leave your debt for the moment, opting instead to invest the extra cash.

Before you decide to divert your savings away from debt, the one rule you need to remember is to always make the minimum repayments on all of your debt! Once you are nailing this, you can start to consider whether you should pay off the debt or invest.

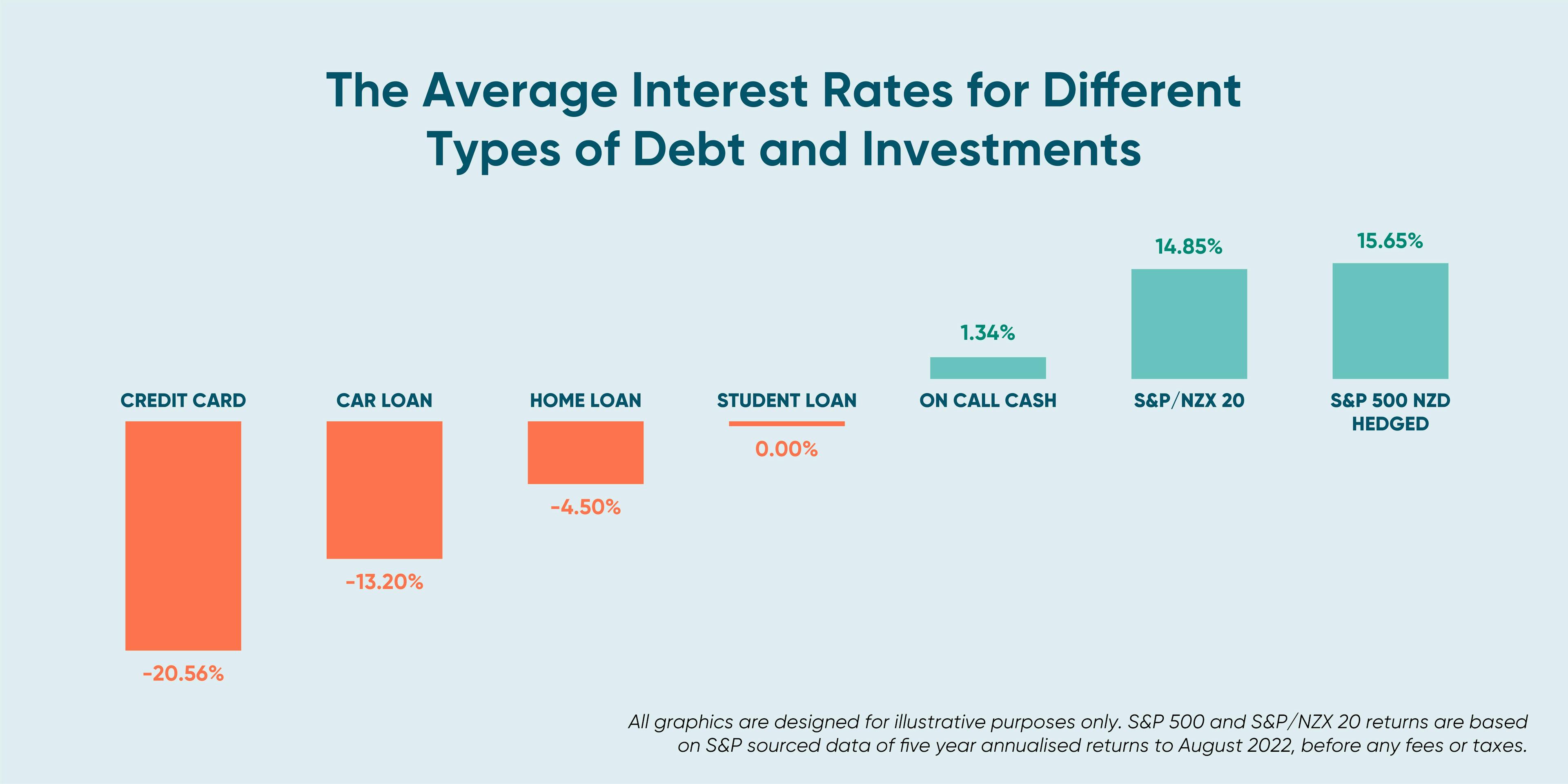

The key thing to consider is the debt’s interest rate and the rate of return on the investment you are considering. If the potential returns on your investment are higher than the debt’s interest rate, you should prioritise investing.

In NZ, the interest rate on student loans is 0% – unless you are overseas for more than six months at which point it will typically be 4%+. Whilst in NZ on PAYE, your minimum student loan repayments are automatically deducted out of your income on pay day.

For most their student loan is interest free, so putting money towards your investments instead of extra repayments would be a logical strategy. Why? The likely long term average return on investing is greater than the 0% interest rate on the student loan debt.

Credit cards have their place for general purchases, assuming that the card has minimal fees and you always pay off the debt before it incurs interest. If you have a persistent credit card balance, however, then this is likely incurring interest at around 20% p.a., or around 13% p.a. if you have a low-rate card. Any personal debt with such high interest rates should be paid off as your first priority.

It is highly likely that the long term returns on investing will be lower than the interest rate on a credit card. Even if your expected return on an investment is higher than your credit card rate, there are a number of risks that make this impossible to guarantee. The money you’ll save by paying down your credit card — thereby avoiding extra interest — is guaranteed.

The same principle applies to considering whether to repay a home loan, car loan or personal debt. When assessing these types of loans versus investments or savings, ask yourself this: “is my expected return higher from investing than my debt’s interest rate?”

If you are thinking about your own home and the dream of being debt-free, it’s also important to consider your time frame. Most home owners know they are in for the long haul – either repaying their property over 15+ years or relying on property growth to maximise their equity before an up-size.

If you are comfortable with this approach and see the value of having your eggs in more than one basket – it’s likely you would achieve a good outcome from investing for the longer term rather than repaying extra to the bank to save ~4% p.a. interest.

While the method above is the most practical way to choose whether to pay off debt or invest, there’s undoubtedly an emotional component to this decision. Some of us may be more risk-averse and the burden of carrying debt can affect your peace of mind.

If you’re not unsettled by either option and are simply trying to come out ahead, then meeting the minimum repayments on low interest debt and investing the extra money can be the smart approach to building wealth and achieving your life goals.

Credit card debt hanging around? You can compare credit cards here.

Reverse engineer your goals by starting with the bigger picture and breaking it down. Want to know m...

Catherine Emerson

19 January 2020

How to Set Up an Emergency Fund

We never know what life can throw at us financially, so we need to be prepared when big expenses hit...

Dean Anderson

4 August 2025

How to Set and Follow Through With Your 2022 Financial Goals

Do you have financial goals or life goals that you'd like to tackle in 2022? We share our tips to do...

Christine Jensen

28 December 2021

For market updates and the latest news from Kernel, subscribe to our newsletter. Guaranteed goodness, straight to your inbox.

Indices provided by: S&P Dow Jones Indices