Active or Passive Investing: deciding which is best for you

We break down what active investing is, how it's different to passive investing and which is the bes...

Dean Anderson

16 September 2020

For many years, active fund managers have advocated that their ability to pick the winning stocks and the winning times outweighs their high fees. Time and time again the data shows that this method of investing results in underperformance compared to that of simply owning a well-diversified index fund.

Now, there is absolutely a place for an active fund or two in an investment portfolio when following a core satellite investing strategy. But when the data shows that active fund managers continue to underdeliver year in and year out, we’re left questioning why Kiwis continue to opt for active funds to make up the bulk of their investment portfolio.

In recent years we have seen an increasing shift to investing in index funds – with one of the major reasons being the poor performance of actively managed funds.

Actively managed funds employee countless staff in an effort to regularly trawl through the market looking for the hidden gems and avoiding the potential lemons. However, decades of data shows that attempting to outsmart the market is a futile game, with typically more than 85-95% of actively managed funds underperforming their benchmark over a 10-year period according to SPIVA.

Source: S&P Dow Jones Indices SPIVA Scorecard. Data shown as at Dec 31 2021 for the previous 10-year period.

Investors shifting to index funds are opting to remove the risk of picking a poor performing active fund manager, instead opting to lower costs and focus on the longer-term factors they can control.

It is hard work being an active fund manager, with time eventually bringing even star managers back down to earth. Take Magellan, a once $110 billion dollar Australian fund manager, operating a flagship global equity fund that was held in many institutional and retail investment portfolios. A period of internal struggles and market underperformance saw them lose over $25b in funds as investors jumped ship.

Continued poor performance in 2022 has seen the gains from years gone by evaporated, and as at 31 March 2022, their Global Fund has underperformed its benchmark index across 1-year, 3-years, 5-years and now 10-years. In short, investors have paid high fees to get a worse return than simply owning the market through a low-cost index fund.

Data from Stockspot, an Australian online financial adviser, found the 10 largest active global fund managers in Australia, including Magellan, have been consistently outperformed by a global 100 index fund and have ended up 47% behind the Global 100 ETF over the past five years.

This comes despite the past two years being a period of higher volatility and higher dispersion (the range between the best and worst-performing stocks), conditions that active managers would often tout as the time when they will create the most value for their investors.

Warren Buffett famously said that when the tide goes out, you’ll see who’s been swimming naked and right now, active fund managers are high and dry. Because despite these ideal conditions, the results of the annual SPIVA scorecard for US fund managers show that 2021 was the third-worst year on record for active managers.

While in any single year, research indicates that typically 50-60% of active funds will underperform their relevant index benchmark, over the longer term this figure trends up to 80-95% - as it is hard to repeat one year's success year on year on year.

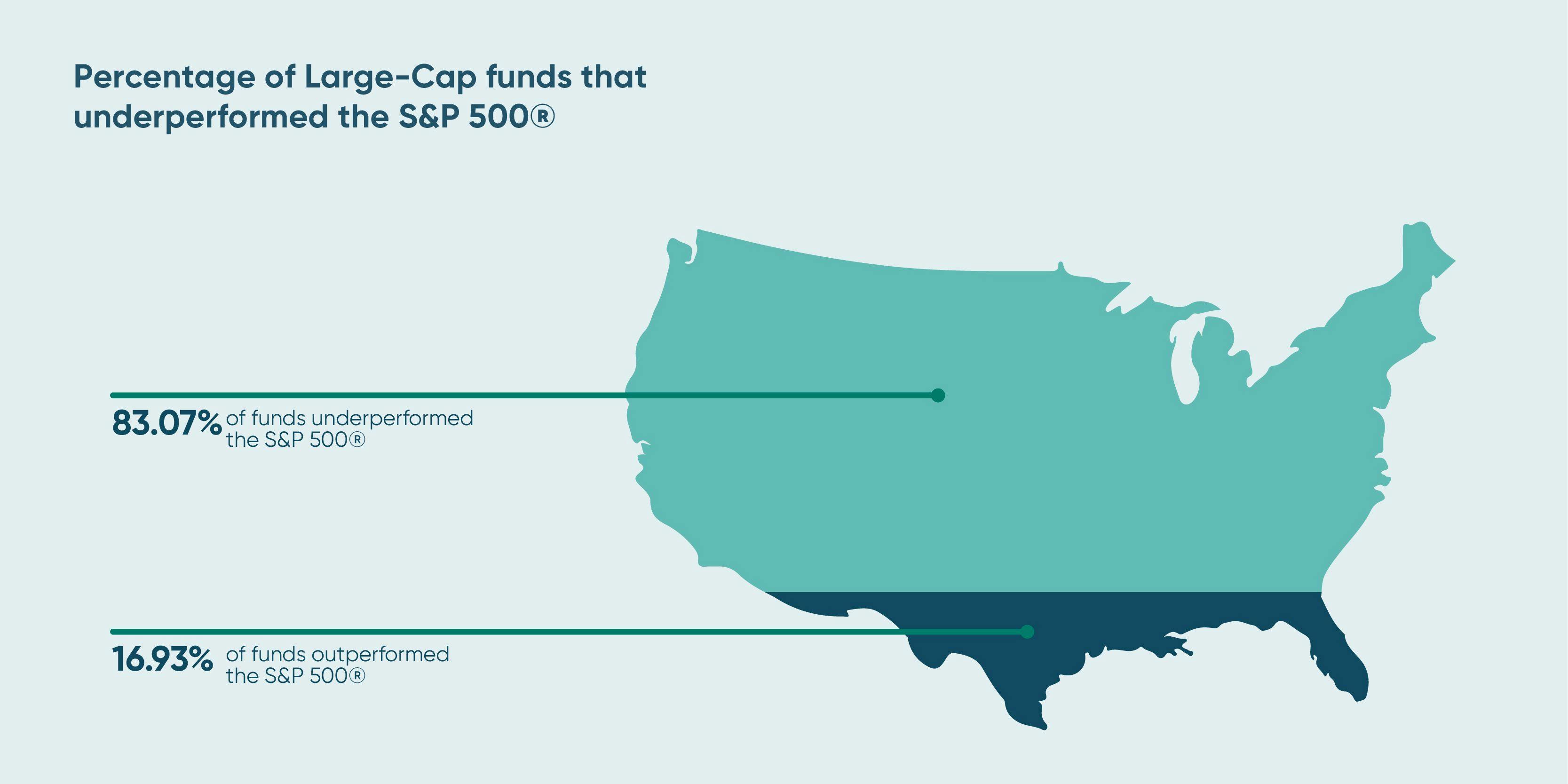

However, 2021 was a particularly difficult year as 80% of all U.S. active fund managers underperformed. Worse yet, 85% of large-cap active fund managers, those investing in the area of the big names like Microsoft and Apple, lagged the globally renowned S&P 500 index. This made 2021 the second-worst year for large-cap managers on record.

S&P Dow Jones Indices’ SPIVA (S&P Index Versus Active) scorecard, first published in 2002, has become the industry’s de facto scorekeeper of the relative performance of active managers. Of course, an investor shouldn’t make a decision based on a single year of data, but with 21 years of history we see a clear pattern, in just 3 of 21 years has a majority of large-capitalisation active managers outperformed the S&P 500!

The numbers don’t lie. Over time, active fund managers are no more skilled at protecting your investment in a downturn than they are at adding value when the market is rising. If active fund managers cannot deliver outperformance over the long term, you have to question what - if any - value they are adding.

Active or Passive Investing: deciding which is best for you

We break down what active investing is, how it's different to passive investing and which is the bes...

Dean Anderson

16 September 2020

7 Things to Consider When Choosing the Right Index Fund

There are hundreds of indices and many different funds available, so how do you choose the right ind...

Dean Anderson

10 June 2020

Why Past Performance is No Indicator of Future Returns

We’ve all heard the disclaimer “past performance is no indicator of future returns” thrown around or...

Chi Nguyen

9 December 2021

For market updates and the latest news from Kernel, subscribe to our newsletter. Guaranteed goodness, straight to your inbox.

Indices provided by: S&P Dow Jones Indices